Housing Bust 2.0?

Posted May 20, 2022

Chris Campbell

Is the Fed crashing the housing market… again?

According to colleague Jeffrey Tucker, the answer is obvious: yes.

We invited him to lay out his case below -- and show how he believes it could all play out.

Before we go there…

Another colleague, Jim Rickards, just “broke rank” with the Washington elite and released a pretty shocking video.

It contains a 153 stock “kill list.” If you own any, says Rickards, “Sell these stocks immediately, today if possible.”

If Jim’s right about this list, I doubt anyone on Wall Street would want you to see this.

That’s why I’m sharing it here today.

Because come tomorrow morning it could already be too late.

Click here to see Jim’s message now.

And read on.

The Fed Is Crashing Housing, Again

Jeffrey Tucker

Back in 2007, the driving ethos was that the housing market could never, under any circumstances go down in total. Prices are entirely local and determined by supply and demand. This is why so many top minds in that year were very hard core: there is no bubble. All fundamentals are strong, they said.

Then of course, everything fell apart, dragging financials down too. From which one might assume that we would learn. If the liabilities are bundled without regard to risk profiles, and traded as securities, then the housing market also becomes as vulnerable as any paper financial product. These days, however, it seems like this lesson wasn’t a lesson at all.

The Buyer of Last Resort

After the epic crash, the Fed became the buyer and holder of trillions in refuse from the calamity. It has worked for a decade to clean up its balance sheet but never really succeeded for fear of causing recession. In February 2020, the Fed owned $1.4 trillion in mortgage-backed securities. It had every intention of dumping these out of its portfolio, thus dialing market liquidity it was providing to market.

Then suddenly, the great virus arrived and Congress went wild with spending. Next thing you know, the Fed’s portfolio of mortgage-backed securities ballooned to $2.7 trillion. They had gone shopping, paying with newly printed money. Wonder of wonders, the housing boom started all over again. It was history on repeat.

Here we are, two years later, with a vastly more complicated problem. Inflation is soaring due mainly to the trillions in hot money dumped all over the country to subsidize lockdowns. Supply chain breakages make that worse. The forced recession of March and April 2020 never really went away. All that has changed is the ability of the federal government to cover it up. Now the numbers are starting to reflect reality, and a recession is upon us.

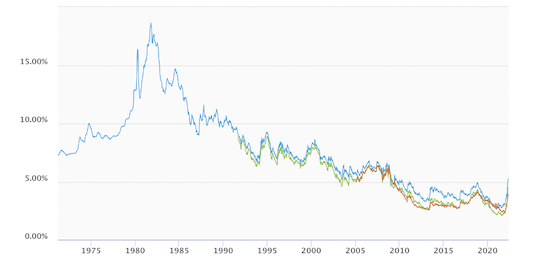

In the middle of this mix of inflation plus recession, we could experience something new: a housing demand-based bust in the middle of a period of high inflation! Thirty-year rates rose above 5% in April for the first time in ten years. Here is a ten year chart.

This small change (there is nothing at all unreasonable about 5% in 30 years) has caused a huge and sudden change in mortgage applications and the drive to build more and more.

Here is the same chart in the context of 1970 to the present. If we really are going back to the 1970s, there is a long way to go before reaching a historically justified equilibrium.

Mortgage applications have already declined 12%. They are 15% lower than the same time last year. Keep in mind, too, that housing prices are up 20% year-over-year, which makes small changes in the rate extremely meaningful for financial decisions.

Let’s say there is a housing bust, even a dramatic one. How does that play out in an environment of very high inflation for everything else? It all depends on how one weighs the housing sector in the construction of the index. It could drag it down for sure but not eliminate it.

In any case, we are nowhere near that point: housing plus utilities inflation is right now still running 12.1%. It’s likely that the next housing bust will take a different form: dramatically declining demand in the context of ever higher prices.

Housing: The Paradigmatic Case

It’s been so long since we’ve experienced “stagflation” that we’ve lost a picture of what it feels like. Normally, a depressed economic environment comes with lower prices. Higher prices we’ve tended to associate with economic booms sector by sector. We almost cannot conceptualize an environment that is at once deeply depressed, with limited demand and productivity, plus rising prices.

We can see how this plays itself out in the housing market. Let’s say that mortgage demand continues to fall dramatically. People choose to rent, or stay put, or otherwise stay out based on their risk aversion in the face of the high costs of financing at the high costs of the asset itself. The large companies that have been buying in lots also pull back. At the very same time, prices are still rising.

What is going on here? And how is this possible? Here is the core of the answer that these days people seem unwilling to accept: the dollar is being systematically devalued. This happens regardless of the supply and demand for goods and services. The phenomenon is entirely traceable to a different form of supply and demand: for money itself.

It is too easy to forget that money is a good, like anything else and subject to economic laws. We are being prompted daily to remember this, but we’ve lived so long in a relatively price-stable environment that people have a hard time understanding this.

For most of our lives, money has seemed like a neutral thing, something to use for calculation and exchange and nothing more. Now it has taken on a life of its own, moving down in value regardless of changes in the demand for goods and services.

In short: this housing bust will not look like the last one. It will be an industry depression, plus inflation. That’s enough to really play with one’s mind. The root cause, however, will be the same: expansionary monetary policy from the Fed enacted to stop the market from responding properly to the conditions of reality.

Money Finds a Home

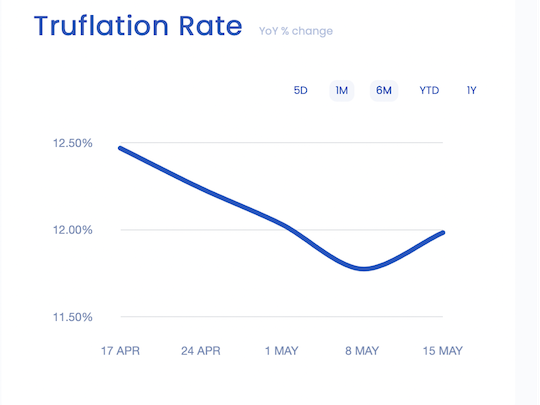

While we’ve yet to see any real softening in the pace of increases in housing prices, and may not at all, the real action has shifted over the last month, from housing to transportation. If you have booked a plane ticket recently, you know this. Transportation costs in general, including the gas you put in your car, are rising 20.5% right now. That’s the fastest sector in the index that is still rising 11.6%.

And by the way, while the overall index dropped in its rate of increase last month, that direction of change has stalled. It is now rising again. Here is the one-month rate of change:

We are entering into a new economic environment, one we will not recognize. The old rules will not apply. We’ll see and experience things as never before. They will be extremely disorienting. And vast swaths of the population will not know enough to understand what is to blame. That’s exactly what the Fed wants. These people will hide as long as possible.

Regards,

Jeffrey Tucker

For Altucher Confidential