I Went Broke Twice, Here’s What Saved Me

Posted November 28, 2023

Chris Campbell

I didn’t want to invest money. I didn’t want to be involved in business.

I wanted to write a novel. I wanted to be a writer. When I was in graduate school for computer science I got a stipend of $1,000 a month. It was the most money I had ever seen in my life. But I failed at it because I wanted to be a writer and not a computer guy.

Every day when I woke up the first thing I would do was write 3,000 words.

I was in graduate school then but I stopped going to all my classes. I continued this practice of 3,000 words per day for over 30 years, and sometime during the pandemic I stopped doing this.

Graduate school threw me out and my friend, Merrick Furst, who was the dean of students at the graduate school had to write me a letter saying when I got “more maturity” I would be invited back.

He still reminds me of this.

I have given him chess lessons for the past 30 years. (I am not sure he has gotten better but we always have a fun time) and sometimes I will bring up what I always bring up (“you threw me out!”) and he brings up what he brings up (“you can always come back!”) but I never do.

I couldn’t publish any books.

I wrote four novels and dozens of short stories. I would send them out to 40 agents, publishers, and magazines. I’d calculate how much money I would make.

I’d be rich! I didn’t publish my first book until 14 years after I started writing every day.

I wish I had read my book, Skip the Line back then. I would’ve published much faster. But, of course, I had to start publishing books before I could write Skip the Line.

I have 1,000s of form rejection letters to show for all the work. And, perhaps, I “paid my dues” as they say. Everything was horrible but I really wanted it. More than anything else ever. Writing is the only activity I have done consistently for over 30 years.

I started writing because I felt I was ugly and I needed to stand out in some way (write a great novel!). And, in fact, I was right. My wife, Robyn, sought me out because she loved my book, Choose Yourself. Mission accomplished.

Sold a million copies, but more importantly, got me a wife.

(But I still felt the need to keep impressing her. Here’s a picture of me and Robyn shortly after we met. I figured I could impress her by saying, “Hey, let’s hop on a plane and go to Peter Thiel’s birthday party.” I’m not sure she was impressed but I was happy she went with me.)

After starting (reluctantly) my first business (nobody knew how to make a website in the 90s and I did), I started to invest.

Here’s an article in Newsweek from 1996 about one of my first (and most fun) websites that I built:

I thought I must be smart since I sold a business. I was so smart I could now invest my money.

Well, as I wrote about many times, I didn’t know how to invest. I went broke. I lost my home. I lost everything. I lost my mind for a while.

But I thought: I need to figure this out. I need to know how to invest.

So just like I did when I was writing, I immersed myself in investing. I read every book I could find. I spoke to many investors, I studied my mistakes, I experimented, I analyzed, I studied again and tried to fix my problems, I read more, and I experimented more.

Investing is not like learning writing, or learning computers, or learning chess. When you lose, you lose money, you lose your freedom, your ability to live.

And I was losing big.

I had worked hard for so many years to build a business. And it was a good business. And I sold it and made money. And all of those years of 20 hours a day of work I flushed down the drain in a few months. I went broke.

I thought I had won the lottery but how many people win a lottery twice? Nobody. I was a dead man walking. I was destined for depression. I would look at my babies and think I ruined their future.

So I immersed myself in investing. It was the source of all my pain but I kept thinking, “I should be good at this”. It combined many of my interests. There’s a game-like aspect of investing. There’s a heavy computer component. And I even brought my writing into it when I started writing for various investing sites back in 2002.

I noticed that most professional investors were not bad, but they were not good either. They worked for big investment companies, emulated the style of those companies, didn’t really study the history of investing, and ultimately became solid, but mediocre investors.

That was true then and maybe even more true now. Everyone relies on newspaper headlines to give them advice on what to invest in. Too late. You have to find the investments and the strategies before the newspapers do.

EVERY investment style works. But you have to know how to apply them.

Value Investing

People think they can read a book about Warren Buffett and then learn how to value invest. This is the most difficult form of investing.

The idea is to buy a stock that is trading very cheap relative to their earnings.

For example: if Exxon is trading for $100 and they have profits of $10 per share then that is a P/E of 10.

That means their “earnings yield” is 10% ($10 / $100). Since 10% is significantly higher than federal interest rates of 5%, then Exxon might be a value play.

“Might” is the keyword.

You have to ask: what is the earnings yield of other oil companies? If one is 15% is that a better investment? How stable is that earnings yield? What are the risks that oil is taken over by solar power or batteries? How are they dealing with that risk?

Will that 10% earnings yield go up or down in a recession? Is this recession-proof? Does Exxon or XYZ oil company have a consistent dividend? When did they last move that dividend down?

All of this is incorporated into the risk and how you compare the earnings yield to the federal interest rates (which is considered riskless so that is the benchmark value investors use when evaluating the risk versus the reward).

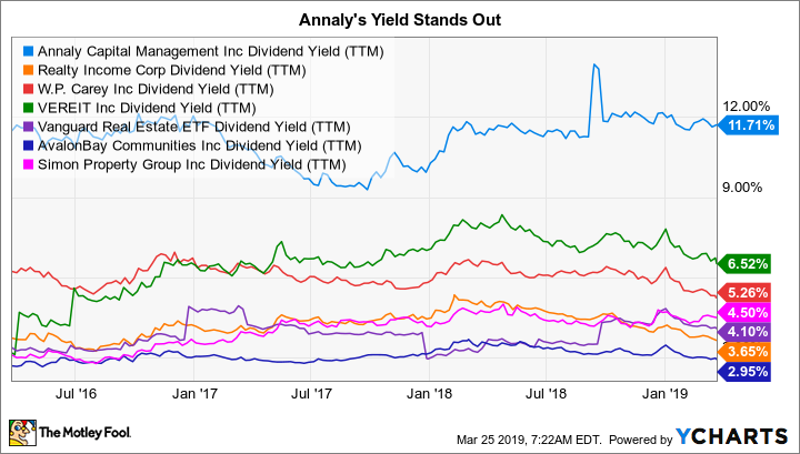

An example value play that I am looking at right now is Annaly Capital Management, Inc. (NLY).

They are currently at a several-year low so I want to understand if that decline in value is rational or if is it simply because all stocks have declined and perhaps this one a little more.

The dividend is 12% (very good!) and the forward P/E ratio is about 7 (very good!).

They own mortgage-backed securities (very bad with higher interest rates!) but the MBSs are backed by the government (very good!) and the Fed has stopped (for now) raising interest rates (very good!). They lowered their dividend (very bad!) but they would’ve lowered it more if their business was truly at risk.

Annaly’s yield is higher than its competitors but this is not necessarily a good thing. Is there a reason for the yield to be so high (e.g. are they buying riskier assets?)? If the answer is “yes” then it’s not a buy. If the answer is “no” then it’s a HUGE buy right here.

I look up which institutions have been buying shares. Blackrock, Geode, Millennium, and others have added shares this past quarter (very good!).

I am not officially recommending this stock but this is the beginning of what I look at. I also want to see how they performed in 2008 (I bought them in 2008 so I have a long history with the stock) and other periods of increased rate hikes.

Growth Investing

Growth investing is not the opposite of value investing as many seem to think.

In fact, growth investing is a subset of value investing.

Let’s take an extreme of value investing, what Warren Buffett likes to call “cigar butt investing”.

A cigar butt is a cigar you see on the ground and you can pick it up and it still has one last puff in it.

When Buffett bought shares for the first time in a little-known shirt company called Berkshire Hathaway in the 60s, he was doing cigar butt investing.

How come? Because he thought liquidating the factories would give him more money than the entire value of the company. He thought that Berkshire Hathaway was riskless because worst case he could buy the whole company and liquidate it and keep the extra money.

It’s rare to find a good cigar butt stock, but in the 60s it was possible, in 2002 and 2008 it was possible. In March 2020 it was possible, and in the 1930s, when Buffett’s mentor, Ben Graham, was doing it, it was possible.

Fine.

Growth investing is sort of like this but you use math to find the cigar butts.

You find industries that are growing exponentially. You look for the stocks in those sectors that might have declined because of market conditions. You filter to find the ones with good management teams and a growing group of hedge fund investors.

You buy a basket of these stocks since nobody knows who the winners will be.

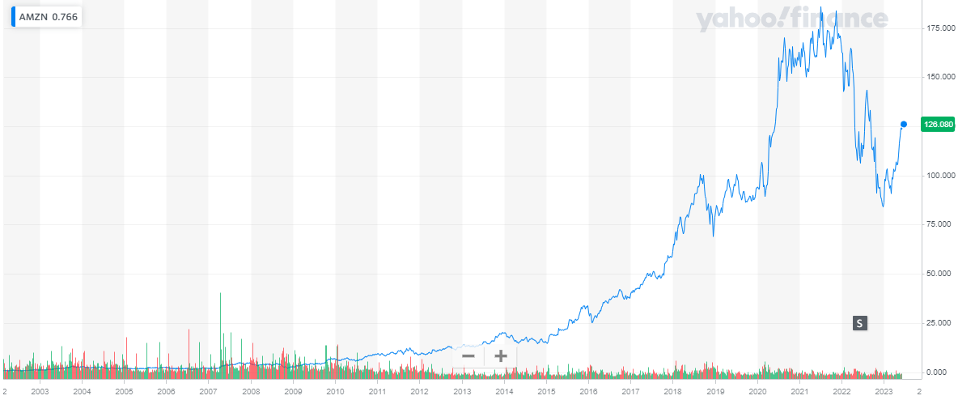

We knew in 2002 that the Internet was growing exponentially in users. But we also knew a lot of internet companies were BS. Hard to pick the winners. No problem, you could’ve had 10,000 losers but if you put $1,000 into AMZN you would’ve made millions.

Without splits, $1 in AMZN would be around $120,000 today. Amazing!

AMZN was deep value but nobody knew it. Only people who said, “The internet is growing exponentially” AND “I need to buy a basket of these stocks” AND “It doesn’t matter what their earnings are” (AMZN had never made a dollar at that point) because it’s growing so fast they will eventually have billions in earnings.

AMZN had $57 Billion in EBITDA last year.

Well, what are the exponentially growing industries now?

AI, Genomics, Electric Cars, Solar power, Robotics, 3D Printing, Crypto, etc.

Exposure to these is a great bet.

Other Investing Strategies

I always write more than I plan to write about each subject. One of these days I will do a course on all the different categories of investing and what might be good picks from each category.

But we covered the two main categories here (barely, but we covered them): value investing and growth investing.

Next up would be options strategies: selling puts, buying condors, selling volatility, buying strangles, etc.

Then perhaps merger arbitrage, convertible arbitrage, quantitative arbitrage.

Then quant investing in general, PIPE investing, crypto investing, index investing, microcaps, and several other strategies.

Plus, there are other aspects of investing that are critical to know: money management, mindset, networking, etc.

I’d like to do a course on this. Write in if you’d like to see such a course.

I would say it took me about 2 years of immersive study to become a break-even investor at day trading. Even a profitable one. But it was too stressful.

And it took me about ten years of non-stop immersion in investing to become a VERY profitable investor.

But I had nobody to really learn from. I had to teach myself and I learned bit by bit. With the right guidance, I am sure becoming a successful investor could be learned much more quickly.

But if you’re in graduate school while you are reading this, please don’t get kicked out. I really missed that $1,000 a month stipend when I lost it.

And, Merrick, I’m sure I’ve already told you this but I forgive you for throwing me out of school.

I deserved it.